- Services

- Accounting and Tax automation

-

-

InvoiceProxy

Seamlessly switch from paper to electronic

We offer you the experience of fully data-driven electronic invoicing, with the security of the infrastructure provided by the National Tax and Customs Administration (NAV).

More…

-

TaxConsole

Automate your Invoices with TaxConsole

Our TaxConsole application allows access to NAV’s digital services directly from your computer.

More…

-

-

- Accounting and Tax automation

The topic has been dealt with extensively in the profession, and therefore it is widely known that only 50% of the local business tax (HIPA) previously declared on the tax return must be paid by micro-, small- and medium-sized enterprises (SMEs) who submitted a declaration to this effect by 25 February 2021.

As explained in details in our earlier newsletter, there were a number of interpretation difficulties in connection with Government Decree 639/2020 (hereinafter: the “Decree”), which granted SMEs a 1% cap on HIPA and a 50% reduction of the tax advance. The biggest difficulty was to determine to what extent, in the application of the Decree for the classification of SMEs, taxpayers must follow the provisions of Act XXXV of 2004 on small and medium-sized enterprises and supporting their development.

As known, Section 1 of the Decree provides allowances for taxpayers that satisfy the conditions for being qualified as micro-, small- or medium-sized enterprises, as defined in the Act on SMEs, with the exception that in their case, the threshold of net revenue or balance sheet total is not EUR 50 million or 43 million, but rather HUF 4 billion. On the basis of the information provided by both the National Tax and Customs Administration (NAV) and the Municipality of Budapest, all conditions under the SME Act must be fulfilled to qualify as SMEs, with the exception of the HUF 4 billion threshold.

In practice, this would have meant that the “two-year rule” according to Section 5 (3) of the SMEs Act would have been applicable to the eligibility for the allowance (if the values calculated for classification as an SME, on an annual level, exceed or fall behind the employee headcount and financial thresholds, then the company only loses or receives the status of SME in case the values exceed or fall behind the relevant thresholds in two consecutive reporting periods).

An information letter issued by the Municipality of Budapest came into our possession a few days ago, which declares that in the classification as an SME according to the Decree, all conditions prescribed in the SMEs Act must be fulfilled, with the exception of the HUF 4 billion threshold, which – by its nature – excludes the applicability of the “two-year rule” of the SMEs Act. This means that, for the purposes of qualification as an SME, the data of the last consolidated financial statement, or in the absence of a consolidated financial statement, the consolidated data of the last financial statements of the enterprise and its partner and affiliated enterprises must be taken into consideration.

The initial confusion is therefore slowly clearing up; however, what can those businesses do that on 25 February 2021, the deadline for submitting their declarations still considered themselves as large companies, and therefore have not submitted a declaration, but – on the basis of the legal interpretations that have since surfaced – actually fulfill the criteria for classification as SMEs?

- On the one hand, by submitting the 21NYHIPA form subsequently, within 15 days, as well as a justification request to the local authorities to provide proof of their business premises, they can request a 50% reduction of the HIPA advance,

- on the other hand, until the date on which the HIPA advance is due (according to the main rule, 16 March and 15 September), they may submit an application for the reduction of the tax advance to the local authorities, with a view to the fact that the tax advance is to be paid on the basis of the data of the previous period, however, according to their calculations, their tax liability will not reach the amount of the tax advance payable on the basis of the preceding period.

It is important, however, that while in the case of a justification request, it must be proved that the failure to submit the declaration occurred do to reasons outside the company’s fault, in the request for the reduction of the tax advance, the applicant must demonstrate the available information and business plans relevant to the HIPA calculations, and then calculate the amount of the expected tax liability. Due care must be exercised when preparing and submitting either the justification request or the request for the reduction of the tax advance, in order to avoid the rejection of the former or a default interest imposed for not being entitled to the tax reduction in the letter case.

We hope that you found our summary useful. If you have any further questions in connection with this topic, we are at your disposal.

VAT rules on temporary agency work to be amended from 1 April

As discussed in our newsletter on the autumn tax package, subject to the decision of the European Commission, the reverse charge rule of the VAT Act will be amended in case of temporary agency work, meaning that it can no longer be applied with the exception of temporary agency work in the construction industry. The essence of the reverse charge mechanism is that VAT is not charged and paid between between two VAT subjects registered domestically (provided that they have no legal status under which VAT payment cannot be claimed from them), because the buyer is required to settle the VAT with the tax authority (NAV) in its tax returns (as payable – and, if it is entitled, as deductible – VAT).

On the basis of the autumn tax package, the new legislation will enter into force on the 30th day after the Minister of Finance declares in the Official Gazette (Magyar Közlöny) that the EU has refused to extend the derogation period despite Hungary’s request. In view of the fact that this happened in Ministerial Decision no. 1/2021 PM, published on 2 March 2021 in issue no. 33 of the Official Gazette, from 1 April 2021 the reverse charge can only be applied in case of temporary agency work in the construction industry that is related to such construction work qualifying as the handing over of real property or the supply of service, as defined in Section 10, point d) of the VAT Act, aimed at the construction, extension, conversion or other alteration of real property (including demolition). In other words, the reverse charge mechanism can last be used in case of temporary agency work, as well as services provided by school cooperatives and public interest pensioner cooperatives until 31 March 2021 only.

The deadline of 25 February 2021 is just around the corner, by which time micro, small and medium sized enterprises (hereinafter: “SMEs”) may submit their request for the 50% reduction of their local business tax (HIPA) advance.

In our earlier newsletter, we have already discussed that Government Decree 639/2020, promulgated on 22 December 2020 (hereinafter: the “Decree”), on the one hand provides for a 1% cap on the local business tax (HIPA) payable by SMEs in their tax year ending in 2021, and on the other hand, based on a declaration that may be submitted by 25 February 2021, SMEs can also receive a 50% reduction of their HIPA advance. As the above deadline is drawing closer, there is increasing uncertainty related to the practical application of the Decree, and therefore, we intend to concentrate on these in our present newsletter.

Section 1 of the Decree prescribes the HIPA rate capped at 1% for taxpayers that qualify as micro, small or medium sized enterprises, as defined in the Act on SMEs, with the exception that in their case, the threshold of net revenue or balance sheet total is not EUR 50 million or 43 million, but rather HUF 4 billion. This rule – also on the basis of the information published by the National Tax and Customs Administration (NAV) in its bulletin of 19 February 2021 – entails that from the point of view of qualification, all other conditions of the Act on SMEs must be applied:

- for the purposes of the qualification, the data of the last consolidated financial statement – or in the absence of a consolidated financial statement, the consolidated data of the last financial statements of the enterprise and its partner and affiliated enterprises – must be taken into consideration, and

- if the values thus calculated, on an annual level, exceed or fall behind the employee headcount and financial thresholds, then the company only loses or receives SME status in case the values exceed or fall behind the relevant thresholds in two consecutive reporting periods (hereinafter: “two-year rule”), and

- as a general rule an enterprise cannot be treated as an SME if the direct or indirect share of the state or the municipality – based on the capital and on the voting right, separately or altogether – reaches or exceeds 25%.

By contrast, Section 2 of the Decree only makes the 50% HIPA reduction available to those enterprises that satisfy the criteria of having fewer than 250 employees and a maximum of HUF 4 billion revenue or balance sheet total on the basis of the following:

- in case of enterprises required to prepare a financial statement, on the basis of the last approved financial statement, prepared pursuant to Act C of 2000 on Accounting, available on the first day of the tax year starting in 2021, or in the absence of an approved financial statement, on the basis of estimated data,

- in case of enterprises not required to prepare a financial statement, on the basis of the revenue and headcount data of the tax year starting in 2020, and in case of enterprises starting their activities in 2021, on the basis of estimated data.

The difference in the phrasing suggests that:

- while the HIPA rate capped at 1% is only available to taxpayers that qualify as SMEs on the basis of their data consolidated on group level and with the two-year rule taken into consideration,

- the 50% HIPA reduction is available to all taxpayers that individually and only on the basis of the last financial report available on the first day of the tax year starting in 2021 – or in the absence of the above, on the basis of estimated data – fulfil the criteria of having an employee headcount of less than 250 persons and a revenue or balance sheet total not exceeding HUF 4 billion.

It is important to be aware of the fact that, in its information bulletin of 5 February 2021, the Municipality Government of Budapest expressly prescribes as a condition of the 50% reduction of HIPA that the taxpayer must satisfy the conditions set forth in the Act on SMEs, in such a way that the upper limit of the net revenue or balance sheet total according to Section 3 (1), point b) is HUF 4 billion. Further, it is also indicative that in its own bulletin, the National Tax and Customs Administration provides the information with general effect that the Decree does not prescribe any different rules than the provisions of the Act on SMEs concerning the aggregation of the data of the enterprise with the data of its affiliates and partner enterprises, and that these rules must also be applied when checking the eligibility for the tax reductions according to the Decree.

On the basis of the above, in order to avoid a fine, it is not worth interpreting the provisions of the Decree related to the 50% reduction of HIPA permissively, and therefore, our recommendation is that only such companies should submit their declarations for tax reduction , i.e. the 21NYHIPA form, until 25 February 2021 that are also eligible to pay HIPA capped at 1%.

We hope that you found our summary useful. If you have any further questions in connection with this topic, we are at your disposal.

In the current, rapidly changing economic environment, it is essential for all businesses to have information of sufficient quantity and quality information for decisions relating to their operations. The source of information in the operation of the business is controlling, which creates the basis for the coordination of planning, accounting, control and information provision by continuously collecting, analysing, processing and forwarding information for the processes of operation according to specified criteria. Controlling thus provides essential information for decision-making in management and supervision.

An effective controlling system ensures:

- the continuous and prompt measurement and control of the undertaking’s performance;

- the development of intelligent planning framework systems determining future operations;

- through the operation of management reporting systems, the organisation’s proper management and flexible active adaptation to changes in the operating environment.

Based on our advisory experience, in case of some businesses, the established controlling functions no longer fit the size and structure of the business, or the complexity of the activity, and in the worst case they are only present as part of accounting tasks.

This experience has led to the establishment of our dedicated Controlling és Management Reporting Department, which is at your disposal with the following services:

- assessing the information needs of management and individual corporate divisions;

- defining key performance indicators (KPIs) in line with the company’s strategic objectives;

- reviewing and, as necessary, improving the processes serving controlling tools, existing controlling tools, and occasionally also supporting the introduction of IT background systems;

- the design, implementation and possible operation of an intelligent controlling system matching the size of the enterprise and the complexity of the activity.

In accordance with your specific needs, our experts provide the above services on the basis of case-by-case orders or in the framework of an outsourced service; thus, we undertake to provide training on the use of our systems, development of the system on a case-by-case basis. as well as its long-term cost-effective operation.

The solutions we use do not require the introduction of a new enterprise resource planning system, as they can process data from any existing system (or systems) or from spreadsheets, and make such data visible with the use of tools that financial professionals are familiar with.

If you are interested in our services, do not hesitate to contact our experts.

At the end of last year, a number of amendments entered into force, by way of Acts of Parliament and Government Decrees, concerning the HIPA-related obligations of businesses for 2021. In our newsletter we give a comprehensive overview of the changes concerning local governments’ tax policy and the allowances for micro, small and medium-sized enterprises, as well as provide information on the abolition of the concept of temporary business activities, as well as changes in the earlier practices concerning the division of the tax bases, auditing and the filing of tax returns.

Restrictions concerning local tax policy

Pursuant to Government decree no. 535/2020 promulgated on 1 December 2020:

- In the tax year ending in 2021, the rate of any local tax (e.g.: HIPA) or municipal tax may not be higher than the rate laid down in the municipal tax decree applicable on 2 December 2020 to the same local tax or municipal tax.

- Local authorities must continue to provide all tax exemptions and allowances available under the rules in effect on 2 December 2020 also in the tax year ending in 2021.

- Local authorities may not introduce new local or municipal taxes for 2021.

Reduced HIPA rates for micro, small and medium-sized enterprises

In the tax year ending in 2021, the rate of the HIPA is capped at 1% for all micro, small and medium-sized enterprises, as defined in Government Decree 639/2020, promulgated on 22 December 2020. This scope of this provision covers enterprises where:

- the total number of employees is less than 250 and

- the annual net turnover or balance sheet total is not more than HUF 4 billion.

With the exception of the HUF 4 billion limit, the regulations of the SME Act apply to the classification.

As a further reduction of their tax burdens, in 2021, micro, small and medium-sized enterprises are required to pay only 50% of their tax advance as due at the given tax advance due date, which reduction is to be entered in the records of the local tax authority without adopting a decision.

Compliance with the above requirements can be determined:

- in case of enterprises required to prepare annual reports, on the basis of the last annual report drawn up and accepted pursuant to the Accounting Act and available on the first day of the tax year starting in 2021, or in the absence of an accepted annual report, on the basis of the estimated balance sheet total, annual net turnover and employee headcount figures;

- in case of enterprises not required to prepare annual reports, on the basis of the annual net turnover and headcount figures in the tax year ending in 2020; and

- in case of enterprises starting their activity in 2021, on the basis of the annual net turnover and headcount figures estimated for the tax year.

The condition of the above reduction of the local business tax advance is that the enterprise is required to submit a declaration via the Hungarian Tax and Customs Administration (NAV), by way of an electronic form, not later than 25 February 2021, to the tax authority according to its registered seat or business premises, to the effect that

- it qualifies as a micro, small or medium-sized enterprise;

- it is entitled to use the amount of the tax reduction according to Government Decree 640/2020 as a temporary subsidy; and

- on 31 December 2019, it was not classified as an undertaking in difficulty, as defined in Section 6 (4a) to (4b) of Government Decree 37/2011, or

- the circumstances according to Section 6 (4a), points c) and d) do not apply to it at the time of the declaration, and further

- if it has not previously done so, it has the address of its business premises registered.

Prices between affiliated undertakings

As from 1 January 2021, the requirement of the Act on the Rules of Taxation to classify contracts between affiliated undertakings will also be incorporated in the provisions on HIPA, and it is stipulated that taxable persons subject to corporate income tax are required to determine their net turnover or net turnover reducing costs and expenses arising from transactions with affiliated undertakings by taking arm’s length prices pursuant to the Act on Corporate Income Tax and Dividend Tax into consideration.

If the difference would reduce the basis for HIPA, it is only possible if the taxpayer has a statement from the affiliated undertaking to the effect that it has increased its HIPA base (the base of foreign tax corresponding to local business tax, corporate income tax or equivalent foreign tax) by the same amount.

The correction may be made in a lump sum or by modifying each component of the tax base separately.

Temporary business activities

As of 1 January 2021, the concept of temporary business activity and the related HIPA obligation will also be abolished.

It is important that the local government on the area of jurisdiction of in which an enterprise is engaged in building construction activities for more than 180 days shall continue to be considered as business premises and thus be subject to the local business tax, provided that all calendar days of the period from the date of commencement of the activity until the date of acceptance of the performance by the client on the basis of the contract between the parties shall be taken into consideration in the calculation of the number of days.

Division of the local business tax base

Due to the change in the definition of permanent establishments and the elimination of the concept of temporary business activity, the rules applicable to the special tax base division method available to businesses pursuing building construction activities have been refined.

In the course of the asset-proportionate division of the tax base between the registered seat and other business premises, the value of leased motor vehicles is to be taken into consideration in proportion to the personnel expenses allocated to the given registered seat and the business premises. So far, the asset value of these vehicles had to be (or should have been) allocated to the settlement where they are typically stored, for which reason taxpayers often opted for a local government with a low tax rate.

Self-revision and tax audits of earlier tax years

It has been clarified that in case the enterprise itself in the framework of self-revision, or the tax authority in the course of an audit, found a tax difference for earlier tax years, then the effect of this difference must be disregarded in the calculation of the local business tax base for the year in which the difference is accounted for. This way it can be precluded that an enterprise would taking certain items into account in the determination of the local business tax base in two tax different years, i.e. it not to increase or decrease the tax base twice.

The new provision continues to allow the taxpayer to take the effect of the detected error into account not in the course of a self-revision, but a tax assessment for the year of the discovery, i.e. not to deviate from the amount of the tax base as shown in its ledger accounts.

Local business tax returns

It was also possible before to submit local business tax returns using the relevant form of NAV instead those of the individual municipalities, but from 1 January 2021, HIPA tax returns may only be submitted with the use of the electronic form of NAV. Excepted from the above rule are private entrepreneurs that do not qualify as sole traders, who may still submit their HIPA tax returns in a paper form, directly to the local authorities.

The local business tax and tax advances must be paid directly to the individual municipalities also in the future.

We do hope that we could be at your service with this information. Should you have further queries, please feel free, to contact us!

In our experience, in 2020, both auditors and the tax authority put more emphasis on the auditing of transfer pricing between affiliates, as well as the end-of-year correction items and the existence of transfer pricing documentations, and a similar approach is also expected for 2021.

In case certain transactions between affiliated enterprises are not properly documented, the tax authority may impose a default penalty, in which case the amount of the fine may be up to HUF 2 million (EUR 5,500) per transaction, and in case of improper pricing, they may also correct the tax base and impose further fines.

Taxpayers concerned must prepare the master file and the country (local) file, and above a certain price also the country-by-country report (CbCR). The deadline for the preparation of the local (country) file is the same as the deadline for filing the corporate income tax returns.

At the same time, many companies use transfer pricing corrections at the end of the year, in case of which problems may easily arise, and therefore, we recommend very careful treatment of this issue and, in a given case, also the involvement of an expert. It is worth thinking over the following:

- was the extent of the targeted and the achieved profit sufficient?

- is the transfer pricing policy created by the group also adequate in Hungary, do the rules established comply with the local requirements?

- are all recognized expenses properly supported?

- is the accounting and tax law treatment of the end-of-year correction items suitable, and are the tax base reducing items properly justifiable?

- are there any difficulties with the timely documentation of the transaction and the use of the proper method of supporting the transfer pricing used?

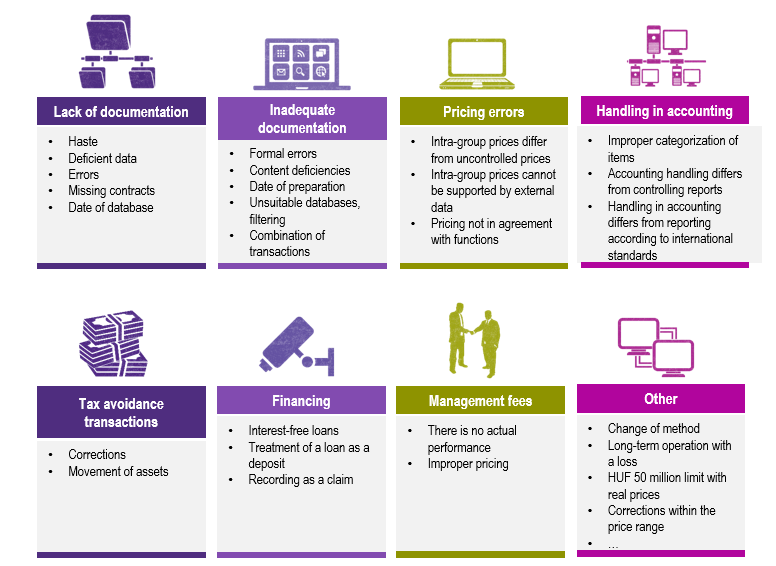

Our experts typically encounter the following, frequently occurring problems and deficiencies:

We do hope that we could be at your service with this information. Should you have any further queries, please feel free, to contact us!